Featured

Table of Contents

In his 4 years as President, President Trump did not sign into law a single piece of legislation that minimized deficits, and just signed one costs that meaningfully decreased spending (by about 0.4 percent). On net, President Trump increased costs rather considerably by about 3 percent, excluding one-time COVID relief.

During President Trump's term in office, federal financial obligation held by the public grew by $7.2 trillion from $14.4 to $21.6 trillion., President Trump's final budget proposal introduced in February of 2020 would have enabled financial obligation to increase in each of the subsequent 10 years, from $17.9 trillion at the end of FY 2020 to $23.9 trillion by the end of FY 2030.

*****Throughout the 2024 governmental election cycle, United States Budget plan Watch 2024 will bring info and accountability to the campaign by analyzing candidates' proposals, fact-checking their claims, and scoring the fiscal expense of their agendas. By injecting an unbiased, fact-based approach into the nationwide discussion, United States Spending plan Watch 2024 will help voters better understand the nuances of the candidates' policy propositions and what they would suggest for the country's economic and fiscal future.

Using Online Loan Calculators for 2026

1 During the 2016 campaign, we kept in mind that "no plausible set of policies could pay off the debt in eight years." With an additional $13.3 trillion added to the financial obligation in the interim, this is a lot more true today.

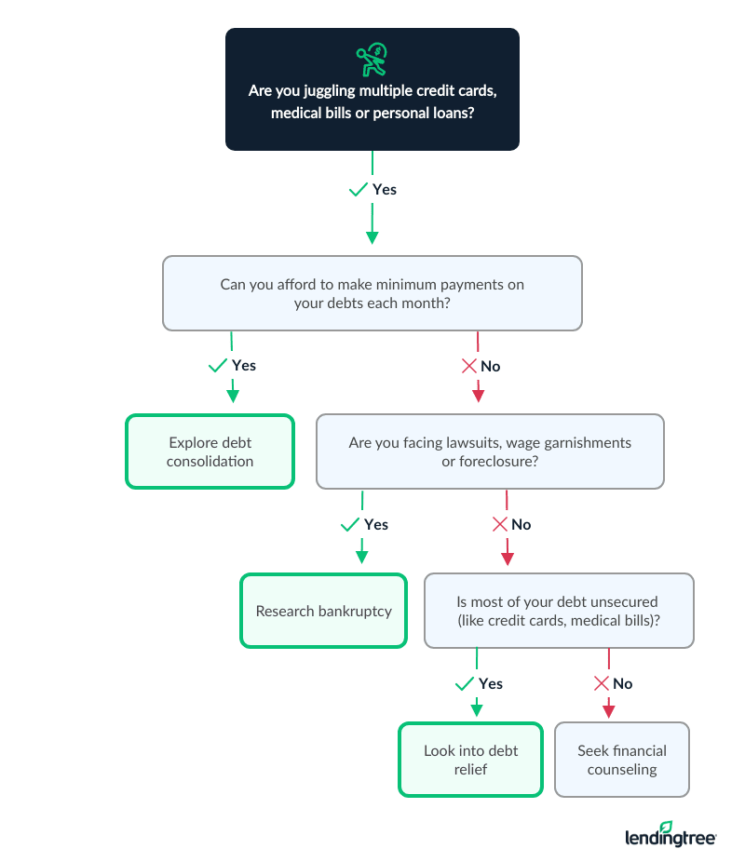

Charge card financial obligation is among the most common monetary stresses in the U.S.A.. Interest grows quietly. Minimum payments feel workable. One day the balance feels stuck. A wise plan changes that story. It provides you structure, momentum, and emotional clearness. In 2026, with greater loaning costs and tighter family budgets, technique matters especially.

Credit cards charge some of the highest consumer interest rates. When balances remain, interest consumes a big part of each payment.

The objective is not just to remove balances. The genuine win is developing habits that avoid future financial obligation cycles. List every card: Current balance Interest rate Minimum payment Due date Put whatever in one file.

Clearness is the structure of every reliable credit card financial obligation payoff plan. Time out non-essential credit card costs. Practical actions: Use debit or cash for day-to-day spending Remove saved cards from apps Hold-up impulse purchases This separates old debt from existing habits.

Enhancing Financial Literacy Through Proven Education

A small emergency situation buffer avoids that setback. Goal for: $500$1,000 starter savingsor One month of important expenditures Keep this cash available however different from investing accounts. This cushion protects your reward plan when life gets unforeseeable. This is where your debt technique USA method becomes concentrated. 2 tested systems dominate personal financing since they work.

When that card is gone, you roll the released payment into the next tiniest balance. Quick wins develop self-confidence Development feels noticeable Inspiration increases The mental increase is powerful. Many individuals stick to the strategy due to the fact that they experience success early. This method prefers behavior over mathematics. The avalanche technique targets the highest rate of interest first.

Extra money attacks the most pricey financial obligation. Decreases total interest paid Speeds up long-lasting benefit Optimizes performance This method appeals to individuals who focus on numbers and optimization. Select snowball if you require psychological momentum.

Missed payments develop costs and credit damage. Set automatic payments for every card's minimum due. Manually send out extra payments to your top priority balance.

Look for reasonable modifications: Cancel unused subscriptions Reduce impulse spending Prepare more meals in the house Sell items you do not use You don't need extreme sacrifice. The objective is sustainable redirection. Even modest extra payments substance in time. Expenditure cuts have limitations. Earnings growth broadens possibilities. Consider: Freelance gigs Overtime moves Skill-based side work Offering digital or physical products Deal with additional income as financial obligation fuel.

How to Find Competitive Financing for 2026

Debt payoff is psychological as much as mathematical. Update balances monthly. Paid off a card?

Everyone's timeline differs. Focus on your own progress. Behavioral consistency drives effective credit card debt reward more than perfect budgeting. Interest slows momentum. Lowering it speeds outcomes. Call your charge card issuer and inquire about: Rate decreases Difficulty programs Promotional deals Lots of loan providers choose working with proactive consumers. Lower interest means more of each payment strikes the principal balance.

Ask yourself: Did balances diminish? A flexible plan survives real life better than a rigid one. Move financial obligation to a low or 0% intro interest card.

Integrate balances into one fixed payment. Negotiates lowered balances. A legal reset for frustrating financial obligation.

A strong debt method U.S.A. households can rely on blends structure, psychology, and flexibility. You: Gain full clearness Prevent brand-new financial obligation Select a tested system Protect against problems Preserve inspiration Adjust tactically This layered technique addresses both numbers and habits. That balance develops sustainable success. Debt reward is seldom about extreme sacrifice.

Building Money Management Skills in 2026Why Consolidate Variable Loans in 2026?

Settling charge card financial obligation in 2026 does not require perfection. It requires a smart strategy and consistent action. Snowball or avalanche both work when you devote. Psychological momentum matters as much as math. Start with clarity. Construct defense. Choose your strategy. Track progress. Stay patient. Each payment minimizes pressure.

The most intelligent relocation is not waiting for the perfect moment. It's beginning now and continuing tomorrow.

, either through a financial obligation management plan, a financial obligation combination loan or financial obligation settlement program.

{kind=link}

Latest Posts

Comparing Rate Reduction Methods for Personal Loans

Improving Financial Literacy Through Effective Budget Management

How to Select a Top Certified Financial Counseling